Is Airwallex actually legit? Or just slick marketing?

That is the real question. So I dug into the fees, the features, the fine print, and the real user reviews. No hype. Just the honest truth before you sign up.

This is what Airwallex really is. What it costs. Where it shines. And the downsides most affiliate reviews quietly skip. Let's get into it. 👇

⚠️ Disclosure & accuracy note: Some links are affiliate links — I may earn a commission at no extra cost to you. This is not financial advice. Airwallex is a licensed payments platform, NOT a bank (no deposit insurance, ATM, or cash). Pricing, features, and eligibility vary by country and change — always confirm current details on the official site for your region.

💱 Open a free Airwallex account — multi-currency, low FX

What Airwallex actually is 🌍

Let me explain it in plain words. Because the marketing can get fuzzy.

Airwallex is a global financial platform for businesses. It helps you hold money in many currencies, get paid from around the world, send money cheaply, and spend with cards. All from one dashboard.

Think of it as a "financial operating system" for a business that deals across borders. Online sellers. Freelancers with global clients. Startups paying overseas suppliers. That is its home turf.

It is built for the modern, borderless business. If your money crosses currencies, Airwallex wants to be the tool that handles it. My hands-on take below comes from testing the real features, not a sales page.

Why it is NOT a bank 🏦

This matters a lot, so let me be clear early.

Airwallex is a licensed payments institution, not a bank. That is a real legal difference. It means there is no deposit insurance like a traditional bank. No ATM card for cash withdrawals. No branch you walk into.

Is that a problem? For most global businesses, no. You are not using it as a place to store your life savings. You are using it as a tool to move and manage money efficiently.

But you should know the line. Keep your core reserves where you are comfortable. Use Airwallex for what it does best: cross-border money movement. I cover the trust side fully in my is Airwallex safe and legit review.

Feature 1: Multi-currency accounts 💱

This is the core. And it is genuinely useful.

With Airwallex, you can hold 20+ currencies in one account. Dollars, euros, pounds, Aussie dollars, and more. All at once. You only convert when you choose to.

Even better, you get local account details in major regions. So a client in the US can pay your "local" USD details. A client in the UK pays your local GBP details. You get paid like a local, not like a foreigner paying wire fees.

For anyone with international income, this alone can save real money and hassle. My multi-currency account guide goes deeper.

Feature 2: Low FX rates 📉

Currency conversion is where banks quietly rob you. Airwallex is built to fix that.

On Airwallex, the FX markup is around 0.5% above the interbank rate for major currencies, and about 1% for others. The free Explore plan even gives access to interbank rates.

Compare that to a typical bank, which can charge 2–4% baked into a bad exchange rate. On large sums, that gap is huge.

That said, "low FX" is not "free FX." There is still a markup. Just a small one. I break down every cost in my Airwallex fees explained ガイド。

Feature 3: Transfer speed ⚡

Slow transfers are a business headache. Airwallex is fast where it counts.

It uses local payment rails in 120+ countries. So many transfers land same-day or within a day, not the 3–5 days of old-school SWIFT wires. Local and batch transfers to those countries are free.

SWIFT transfers still exist for places without local rails, and those carry a fee (around $15–$25) and take longer. But for most common routes, the speed is a real upgrade.

💡 See the FX savings on your own transfers — free to open

Feature 4: Cards 💳

Airwallex gives you corporate cards. Both virtual and physical.

You can issue unlimited multi-currency cards with zero international fees. You spend straight from your currency balances. You set limits and controls per card. Great for teams and ad spend.

There is also a cash rebate: up to 1.5% on USD spend. So your business spending earns a little back. For companies with real card volume, that adds up. See my Airwallex corporate cards guide for the full rundown.

Feature 5: Yield 💰

Here is a nice bonus. Your idle cash can earn.

Airwallex Yield lets your USD balance earn a return — around 3.17% to 3.44% depending on your plan. So money sitting in your account is not dead weight; it works a little.

A fair note: Yield availability and rates vary by region and change over time, and it is an investment feature, not a guaranteed bank interest. Read the terms for your country. But for businesses holding USD, it is a welcome extra.

Integrations & automation 🔌

Airwallex is not just an account. It connects to your stack.

It integrates with tools like Xero, QuickBooks, NetSuite, Shopify, WooCommerce, and Amazon. So your payments, bookkeeping, and sales can talk to each other. There is also an API for developers who want to build payments right into their product.

For a growing business, this turns Airwallex from a "money app" into part of your operations. Less manual work. Fewer spreadsheets.

The honest downsides ⚖️

No tool is perfect. Here is what most affiliate reviews skip.

It is not a bank. No deposit insurance, no cash, no branch. Know the limits.

Support can be hit or miss. Some users report slow responses. For a money platform, that is worth knowing.

Account holds happen. As with many fintechs, accounts can face reviews or holds, especially for unusual activity. Keep your documents clean and your activity clear.

It can feel complex. The power comes with a learning curve. A solo freelancer might find it heavier than needed at first.

Regional fine print. Fees, features, and eligibility differ by country. What is true in the US may differ in the UK or Singapore. Always check your region.

These are real. None are dealbreakers for the right user. But you deserve the full picture. My is Airwallex worth it post weighs them honestly.

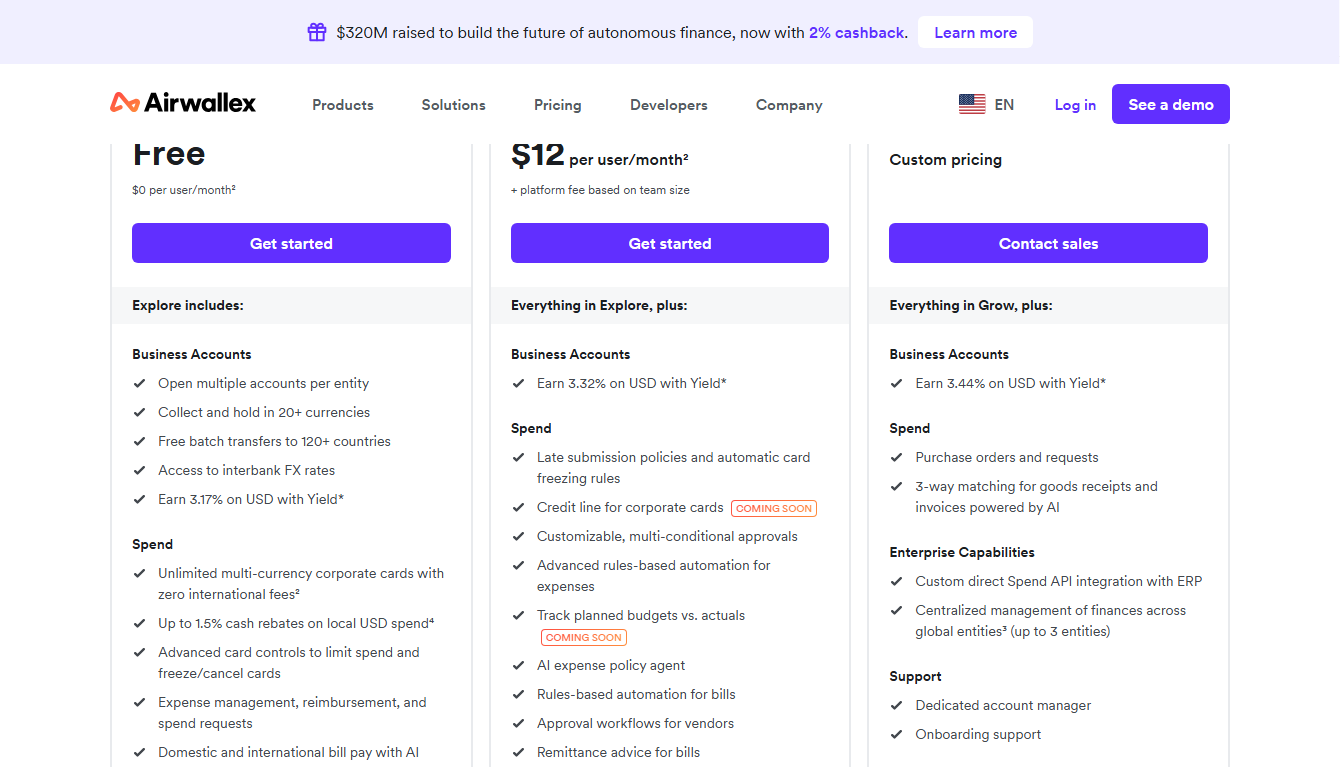

Pricing at a glance 💸

Airwallex runs on three plan tiers. Here they are, checked on the official site in 2026.

| プラン | Price | 最適 |

|---|---|---|

| 🆓 Explore | $0/user/mo | Startups, freelancers, testing |

| 📈 Grow | $12/user/mo + platform fee | Growing teams, automation |

| 🚀 Accelerate | カスタム | Larger, multi-entity businesses |

The free Explore plan is genuinely capable: multi-currency accounts, interbank FX access, free local transfers to 120+ countries, corporate cards, and up to 1.5% USD rebates. For many, free is enough to start. Full breakdown in my Airwallex pricing plans ガイド。

What real reviews say ⭐

I read beyond the marketing. Here is the honest pattern.

Users love the FX savings, the multi-currency accounts, and the speed. For cross-border businesses, those are the headline wins, and they show up again and again in reviews.

The common gripes? Support speed and occasional account reviews. These are the same pain points across the fintech space, not unique to Airwallex. But they are real, and worth setting expectations on.

Overall, the sentiment is positive, especially from businesses that actually need global money movement. The fit matters more than the hype.

Watch my full review 🎥

Prefer video? Here is my honest walkthrough.

Airwallex vs a traditional bank 🆚

Let me show why global businesses switch. The gap is bigger than it looks.

The bank was built for a world where money stayed in one country. Airwallex was built for a world where it does not. If your business is global, that design difference shows up on every invoice and every transfer.

A real cost example 🧮

Numbers make it concrete. So here is a simple example.

Say you receive $10,000 a month from overseas clients, and you convert it to your home currency. With a typical bank charging ~3% FX, that conversion costs you about $300. Every month. That is $3,600 a year, gone to the spread.

With Airwallex at ~0.5%, the same conversion costs about $50. That is a saving of roughly $250 a month, or $3,000 a year. On one simple money flow.

Now add free local transfers, card rebates, and Yield on idle USD, and the gap widens further. For a business with real cross-border volume, Airwallex can pay for itself many times over. My fees guide shows how to push your total cost even lower.

Of course, your exact numbers depend on your currencies, volume, and region. But the direction is clear: less lost to the spread, more kept in your business.

How to open an account 🟢

Getting started is straightforward. Here is the path.

First, check you are eligible. Airwallex serves businesses in many supported countries, and you usually need a registered business entity. A sole trader setup may work in some regions; check yours.

Second, sign up and complete verification (KYC). Have your business documents ready: registration, director ID, and proof of address. Matching, accurate documents speed approval.

Third, once approved, activate your global accounts, issue cards, and connect your tools. Then run a small test transfer to feel the flow.

That is the whole loop. My step-by-step how to open an Airwallex account guide walks every screen and the mistakes that cause delays.

Tips to get the most from Airwallex 🌟

A few things I learned that make a real difference.

Hold, then convert. Do not auto-convert every payment. Hold currencies and convert when the rate or your need is right. That control is the whole point of a multi-currency account.

Use local details everywhere. Give clients your local account details for their region. They pay like it is domestic, and you skip wire fees.

Put idle USD to work. If Yield is available in your region, let idle cash earn instead of sitting flat.

Lean on cards for spend. Zero international card fees plus USD rebates make Airwallex cards a smart default for business and ad spend.

Keep your documents clean. Clear, consistent records reduce the chance of account reviews or holds. Treat compliance as a feature, not a chore.

Who Airwallex is for 🎯

Let me be honest about fit. It is not for everyone.

Airwallex is great for you if:

- 🌍 You get paid from clients or customers in other countries.

- 🛒 You run cross-border e-commerce or dropshipping.

- 🧑💻 You are a freelancer or agency with international income.

- 🏢 You pay overseas suppliers or remote staff.

- 💸 You are tired of losing 2–4% to bank FX.

You can skip it if:

- 🏠 All your money stays in one country and currency.

- 🏦 You need a traditional bank with cash, branches, and insured deposits.

- 🪶 Your volume is tiny and a simple local account already works.

Still unsure? Compare it in my Airwallex vs Wise そして Airwallex vs Payoneer posts.

My honest verdict ⭐⭐⭐⭐

So, is Airwallex worth it in 2026?

For global businesses, yes. Clearly. The FX savings are real. The multi-currency accounts are genuinely useful. The speed and cards are strong. And the free plan lets you start with no monthly cost.

Is it perfect? No. It is not a bank. Support can lag. There is a learning curve. And the fine print varies by region. But none of that is a dealbreaker for the right user.

My rating: 4.4 / 5. A genuinely strong financial platform for businesses that move money across borders. If that is you, it is one of the best tools available. Open the free account and test it on your own transfers.

よくある質問❓

Is Airwallex legit and safe?

Yes. It is a licensed payments platform operating in many countries. It is not a bank, so there is no deposit insurance, but it is a real, regulated company. See my 安全性レビュー.

Is Airwallex free?

The Explore plan is free ($0/user/month) and quite capable. Paid plans (Grow at $12/user/mo, Accelerate custom) add automation and features. See my 価格ガイド.

How much does Airwallex charge for currency conversion?

Around 0.5% above interbank for major currencies, ~1% for others. Far below typical bank markups of 2–4%. Details in my fees guide.

Is Airwallex a bank?

No. It is a licensed payments institution, not a bank. No deposit insurance, ATM, or cash. It is a money-movement and management platform for businesses.

Who should use Airwallex?

Global businesses, online sellers, freelancers with overseas clients, and companies paying foreign suppliers. If your money crosses currencies, it fits well.

Airwallex vs Wise — which is better?

Both are strong. Wise is simpler for basic transfers; Airwallex is deeper for business operations. See the full Airwallex vs Wise comparison.

最後に🏁

Airwallex is not hype. It is a serious tool for serious global business.

It saves real money on FX. It lets you hold and get paid in many currencies. It moves money fast and gives you cards and Yield on top. The honest catches: it is not a bank, support can lag, and the fine print varies by region.

If your business lives across borders, it earns its place. Open the free account, run a real transfer, and judge with your own eyes. That test tells you more than any review.

💱 Open your free Airwallex account today

Affiliate link · Not a bank · Not financial advice · Confirm details for your region

Last updated: 2026. All fees, rates, and features are based on official information from airwallex.com at the time of writing and may change by region. Airwallex is a licensed payments platform, not a bank. This review reflects my own research and honest opinion and is not financial advice.

- How to Open an Airwallex Account in 2026 (Step-by-Step) 🚀 - 6月 27, 2026

- Airwallex Review 2026: Honest Truth Before You Sign Up 💱 - 6月 27, 2026

- MuleRunの活用事例:2026年にAIエージェントを活用する12の具体的な方法🚀 2026年6月23日